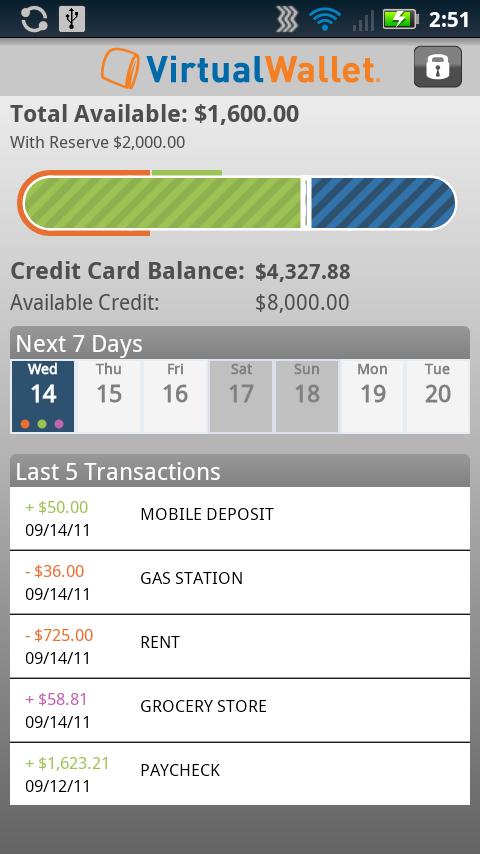

Learning how to do online banking can be a great way to manage your bank accounts. Online banking allows you to do everything from depositing a check to checking your available balance online. You can easily see transactions by time and type. You can even set alerts so you are notified when your balance drops below a particular amount. You can even get notified when a check clears. The options are endless and will help you protect yourself from fraud and other ill-gotten gains.

Online banking is managing your bank accounts via a computer or mobile device

Online management of your bank accounts is the best way to manage your money. Online banking gives you access to all of your money, including your bank accounts, debit cards and investments. Every deposit, every debit card swipe payment, bill payment, paycheck and investment are recorded online. It's easy to check your balance or invest money online. You can also set up alerts for various events, such as when your balance drops below a certain level, a deposit has cleared, or when you have a certain amount of money available.

Online banking offers many advantages. You can access your accounts whenever you want, as long as you have an internet connection. Many people find online banking much more convenient than visiting a local bank branch. It allows you to track your finances from anywhere at any time. You can use your mobile device to deposit checks or transfer money from different accounts. Mobile banking is possible on certain smartphones but not all. You will need an Internet connection and a high-quality smartphone.

It is convenient

Online banking is a popular way for people to manage their finances. Because you can access your accounts 24/7 from any device with an Internet connection, this service is very convenient. This service allows you to make basic banking transactions at any time, saving you both time and effort. Listed below are the pros and cons of doing online banking. To use this service, you must have a bank account and a secure password.

Online banking offers convenience as one of its greatest advantages. Online banking allows you to avoid traffic, long lines and leaving work for the bank. In addition, you can perform all your banking on your own schedule, without a need to rush off to a bank branch. Mobile phones can be used for some banking tasks, such as funds transfers. This option is particularly helpful for working people. Although you don't need to worry about missing important information, it does have its drawbacks.

It is secure

Online banking may have its risks but it's often safer than traditional banking. Many banks offer top-notch security to protect your money. Some offer fraud monitoring free of charge. In today's hacker-happy cyberspace fraud protection is vital. These features should be considered when choosing an online bank.

First of all, avoid using public Wi-Fi networks. The internet has security risks. Hackers are able to hack into your account by keylogging. A VPN is recommended for public Wi-Fi. Also, make sure you use unique passwords. These passwords should not reveal your personal information. You can make your banking more secure by using a unique code for each bank account. You should never use the same password on more than one account.

It can be used to prevent fraud

Safely banking online can help protect your funds. Theft is becoming increasingly sophisticated and banks and financial institutions often have millions of dollars worth of assets. They don't rob branches with guns. Instead, they use sophisticated digital tools and steal personal information to impersonate customers to make purchases and transactions in their name. Ryan Leblond, ESL Federal Credit Union's manager of fraud prevention in Rochester, Minnesota says technology can help financial institutions stay on top of these new trends.

When doing online banking, check when you last logged in, and use historical reporting features to confirm payment and transaction data. Report suspicious activity and regularly check your account balance. Bill Pay can be used to control the distribution of your account number as well as improve electronic record keeping. To avoid malware, it is important to limit administrative rights to financial institutions. These tips can help you avoid identity theft and fraud. Online banking can be used to buy and sell items as well as bank transactions. However, you should always exercise caution.

FAQ

Can I invest my 401k?

401Ks offer great opportunities for investment. Unfortunately, not everyone can access them.

Most employers give their employees the option of putting their money in a traditional IRA or leaving it in the company's plan.

This means that you can only invest what your employer matches.

You'll also owe penalties and taxes if you take it early.

How do I wisely invest?

You should always have an investment plan. It is important to know what you are investing for and how much money you need to make back on your investments.

Also, consider the risks and time frame you have to reach your goals.

This will allow you to decide if an investment is right for your needs.

You should not change your investment strategy once you have made a decision.

It is better to only invest what you can afford.

What is the time it takes to become financially independent

It depends on many variables. Some people can become financially independent within a few months. Others take years to reach that goal. However, no matter how long it takes you to get there, there will come a time when you are financially free.

The key is to keep working towards that goal every day until you achieve it.

Do I need any finance knowledge before I can start investing?

No, you don’t have to be an expert in order to make informed decisions about your finances.

All you need is commonsense.

Here are some simple tips to avoid costly mistakes in investing your hard earned cash.

Be cautious with the amount you borrow.

Do not get into debt because you think that you can make a lot of money from something.

Make sure you understand the risks associated to certain investments.

These include inflation, taxes, and other fees.

Finally, never let emotions cloud your judgment.

Remember that investing doesn't involve gambling. It takes discipline and skill to succeed at this.

This is all you need to do.

How do I know if I'm ready to retire?

The first thing you should think about is how old you want to retire.

Is there a particular age you'd like?

Or would it be better to enjoy your life until it ends?

Once you have established a target date, calculate how much money it will take to make your life comfortable.

You will then need to calculate how much income is needed to sustain yourself until retirement.

Finally, you need to calculate how long you have before you run out of money.

Can I get my investment back?

Yes, it is possible to lose everything. There is no such thing as 100% guaranteed success. There are however ways to minimize the chance of losing.

One way is to diversify your portfolio. Diversification spreads risk between different assets.

You can also use stop losses. Stop Losses allow you to sell shares before they go down. This reduces the risk of losing your shares.

Finally, you can use margin trading. Margin trading allows for you to borrow funds from banks or brokers to buy more stock. This increases your chances of making profits.

Statistics

- 0.25% management fee $0 $500 Free career counseling plus loan discounts with a qualifying deposit Up to 1 year of free management with a qualifying deposit Get a $50 customer bonus when you fund your first taxable Investment Account (nerdwallet.com)

- Some traders typically risk 2-5% of their capital based on any particular trade. (investopedia.com)

- An important note to remember is that a bond may only net you a 3% return on your money over multiple years. (ruleoneinvesting.com)

- They charge a small fee for portfolio management, generally around 0.25% of your account balance. (nerdwallet.com)

External Links

How To

How to properly save money for retirement

Retirement planning involves planning your finances in order to be able to live comfortably after the end of your working life. It is where you plan how much money that you want to have saved at retirement (usually 65). You should also consider how much you want to spend during retirement. This includes things like travel, hobbies, and health care costs.

You don't always have to do all the work. A variety of financial professionals can help you decide which type of savings strategy is right for you. They will examine your goals and current situation to determine if you are able to achieve them.

There are two types of retirement plans. Traditional and Roth. Roth plans allow you put aside post-tax money while traditional retirement plans use pretax funds. It all depends on your preference for higher taxes now, or lower taxes in the future.

Traditional Retirement Plans

A traditional IRA allows pretax income to be contributed to the plan. You can make contributions up to the age of 59 1/2 if your younger than 50. You can withdraw funds after that if you wish to continue contributing. You can't contribute to the account after you reach 70 1/2.

You might be eligible for a retirement pension if you have already begun saving. These pensions will differ depending on where you work. Some employers offer matching programs that match employee contributions dollar for dollar. Other employers offer defined benefit programs that guarantee a fixed amount of monthly payments.

Roth Retirement Plans

Roth IRAs do not require you to pay taxes prior to putting money in. Once you reach retirement age, earnings can be withdrawn tax-free. However, there are limitations. However, withdrawals cannot be made for medical reasons.

A 401(k), or another type, is another retirement plan. Employers often offer these benefits through payroll deductions. Extra benefits for employees include employer match programs and payroll deductions.

401(k).

Most employers offer 401k plan options. These plans allow you to deposit money into an account controlled by your employer. Your employer will automatically pay a percentage from each paycheck.

Your money will increase over time and you can decide how it is distributed at retirement. Many people want to cash out their entire account at once. Others may spread their distributions over their life.

Other types of Savings Accounts

Other types of savings accounts are offered by some companies. TD Ameritrade allows you to open a ShareBuilderAccount. You can use this account to invest in stocks and ETFs as well as mutual funds. You can also earn interest on all balances.

Ally Bank allows you to open a MySavings Account. This account can be used to deposit cash or checks, as well debit cards, credit cards, and debit cards. You can also transfer money from one account to another or add funds from outside.

What To Do Next

Once you have a clear idea of which type is most suitable for you, it's now time to invest! Find a reputable firm to invest your money. Ask family and friends about their experiences with the firms they recommend. Check out reviews online to find out more about companies.

Next, you need to decide how much you should be saving. Next, calculate your net worth. Net worth can include assets such as your home, investments, retirement accounts, and other assets. It also includes liabilities, such as debts owed lenders.

Divide your net worth by 25 once you have it. That is the amount that you need to save every single month to reach your goal.

For example, if your total net worth is $100,000 and you want to retire when you're 65, you'll need to save $4,000 annually.